Cement Sector: Healthy Demand to Cushion EBITDA even as Supply Influx Continues

by Khushbu Lakhotia, Director, India Ratings & Research

FY27 is likely to witness a continued mid to high single digit growth in cement demand led by continued growth in infrastructure as well as housing. With a likely GDP growth of 6.9% in FY27, the cement demand growth to GDP growth multiplier is likely to come in at 0.9-1x

The union budget provides for a 9% increase in the FY26 capex to INR12.2 trillion and an 11% increase in the effective capex (including grant-in-aid) to INR17.1 trillion, which would drive the expected growth in cement demand, given the infrastructure sector forms around one-fourth of the cement demand. This follows a 6% growth rate in effective capex as per FY26(RE). Despite 70% of the budgeted capex already incurred in 9MFY26 (vs 62% in 9MFY25), FY26RE is marginally lower than the budgeted, and the grant-in-aid component is significantly lower. Therefore, while the growth in FY27BE looks higher than FY26RE, the actual growth could be restricted to a single digit.

A key miss in FY26 is the affordable housing scheme, wherein the revised estimate is half of the budgeted estimate of around INR800 billion, affecting cement demand from the segment. While FY27BE is largely on par with FY26BE, execution remains to be seen.

While the budgeted capex for FY27 is in line with expectations, Ind-Ra expects healthy growth in medium-term cement demand from urban infrastructure development particularly in tier 2 and 3 cities, with a proposed allocation of INR50 billion per city economic regions over five years. The cement demand visibility is also aided by announcements, such as a) dedicated freight corridors connecting Dankuni in the East to Surat in the West and b) development of seven high-speed rail corridors, particularly in West and South.

Stable agriculture growth and low inflation are likely to keep rural real wage rate of agriculture in positive territory, supporting rural housing demand in FY27. Further, the income tax cut announced in the FY26 budget and GST rationalisation in September 2025 will improve disposable income.

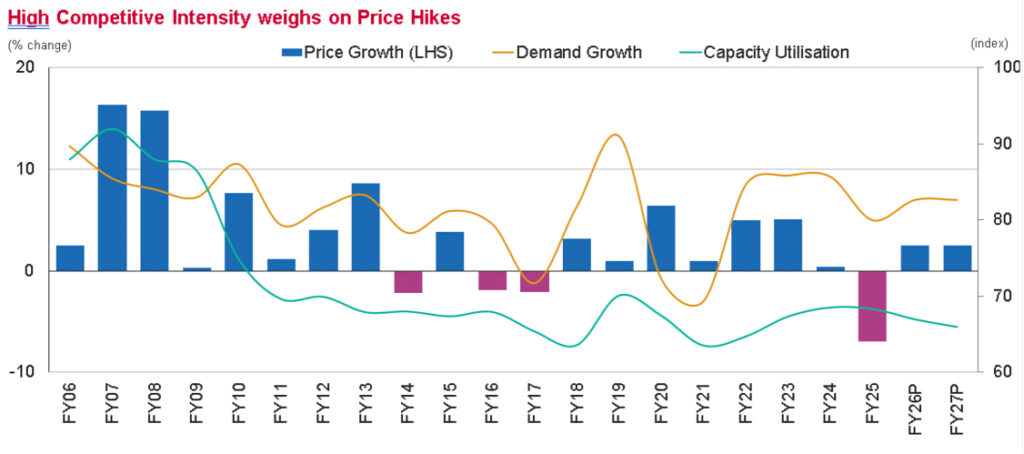

Supply & Market Dynamics: Capacity expansions of around 130 million tonnes (mnt) have been announced over FY26-FY27 on a capacity base of around 615mnt in FY24. Around 75%-80% of the planned expansion is likely to come onstream over FY26-FY27, given the possibility of delays in obtaining clearances, equipment ordering/delivery and adequacy of cash flows/leverage thresholds (particularly for mid-sized players) being the key constraints. However, the pipeline for FY27 is heavy due to which the implied three-year supply CAGR over FY25-FY27 likely to slightly exceed demand growth. The capacity utilisation is likely to remain range-bound at 67%-68%, marginally lower than 69%-70% witnessed in FY24. However, a silver lining is that announced clinker additions are close to the half of the planned cement additions, resulting in clinker utilisations likely remaining higher than the cement utilisations, indicating a higher effective utilisation rate.

North is likely to remain the most balanced region, with capacity utilisations remaining the highest in the country, despite a likely moderation in FY26. Utilisations in the western region are likely to improve due to growth in demand and limited capacity additions. However, competition would be high, given the influx of surplus cement from the south market. The reverse is true for central India where a large pipeline is likely to weigh on otherwise strong utilisations over the near term. Around one-fourth of the planned capex is concentrated in the high-potential eastern region, largely in the form of grinding units. Consequently, the region is likely to witness subdued capacity utilisations in the near term, before demand growth catches up, resulting in a subdued profitability in the region.

The cement industry has witnessed a massive wave of consolidation in the past couple of years. Despite a lull in FY26, the sector could witness further consolidation in the near- to medium term, given that the aggressive medium-term capacity targets of large players are unlikely to be achieved organically with the available resources and a widening gap between leading and small players.

Pricing Environment: After witnessing the sharpest yoy price fall in almost two decades, prices recovered marginally in FY26. After a meaningfully increase in the early part of the year, prices corrected post monsoons and GST rationalisation, culminating into a 2-3%yoy increase in 10MFY26. The pricing environment is likely to remain subdued in FY27 as companies focus on increasing their volumes amid the influx of decadal-high capacities, with hikes restricted to low single digit.

Profitability: EBITDA/mt of cement companies is likely to remain range-bound in FY27, cushioned by the benign input cost environment and continued cost reduction measures taken by sector players. The absolute EBITDA could, however, be supported by the volume growth. The EBITDA of the tier 1 players will continue to outperform the industry average, due to their strong brands, strong market position and cost efficiencies in addition to company-specific cost-saving measures. A recovery in the profitability for the tier 2 players is likely in FY26 given the price hikes in the initial part of the year.

Carbon Emissions: The Union budget of FY27 has provided an outlay of INR200 billion towards the development of carbon capture utilization and storage (CCUS) technologies across five sectors (including cement), which is critical to achieve the long-term carbon emissions in these hard to abate sectors. The allocation for FY27 is modest at INR5 billion, with investments likely to gradually scale up. While its commercial viability of CCUS technologies is yet to be established, this is an important first step given that other levers like alternative fuels, green power, clinker reduction can only contribute to around one-third of the targeted emission reduction for 2070. In October 2025, the government for the first time set mandatory emission reduction targets for 186 cement plants, aiming for mid-single digit reduction in emission intensity by FY27 (compared to FY24 baseline).

Tags

")